2010 Economic Overview:

An improving U.S. economy helped Mexico achieve a strong economic rebound as the country’s economy was well-positioned to benefit trade-wise from the improvement in the U.S. As a reflection, during 2010, Mexico’s market share of total U.S. imports increased to 12.1 percent during 2010 from 11.4 percent during 2009.

The U.S. recovery had a

ripple-effect on Mexico’s export sector, which for the year rose to a record high level, totaling U.S$298.4 billion (30 percent year-over-year growth), derived from a 40 percent increase in oil exports and a 29 percent increase in the non-oil sectors. Mexican exports were favored especially in the manufacturing sector, which accounted for 77.6 percent of total exports.

In addition, Mexico’s current account deficit dropped by more than 30 percent in 2010, when compared to 2009; Mexico’s peso also appreciated by more than 10 percent since the recession. It is worth noting that among emerging economies exporting to the U.S. (Mexico, China, ASEAN countries, the Latin America region), Mexico is the only economy whose export price index declined compared to the previous year: therefore, Mexico’s manufactured goods, compared to other exporters, were more competitive than before. This relative advantage to other emerging economies would draw more investments to Mexico during 2011.

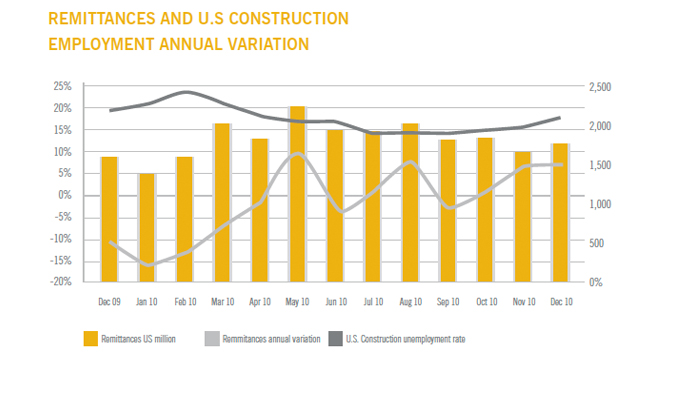

During 2010, remittances (contributions sent by Mexicans living abroad to their families at home in Mexico), which represent 3 percent of Mexico’s total GDP, were at a five-year low.

This drop is mainly attributable to factors in the U.S. including the recovery in employment and the performance of the construction industry, which undermined remittances. The U.S. Latin labor force unemployment rate during 2010 was 12.5 percent compared to 12.1 percent in 2009. These figures are significantly higher than the U.S. unemployment rate of 9.4 percent in 2010 and 9.3 percent during 2009. Consequently, and in spite of a slight increase on the U.S. construction unemployment rate, total revenue from remittances in the year amounted to U.S$21.2 billion, up 0.1 percent over 2009. A potential recovery is expected to materialize during 2011. As of the first quarter of 2011, and for the sixth consecutive month, remittances recorded a growth of 5.8 percent. It is worth nothing that remittances are not an important factor for the homebuilding industry performance as remittances are mainly used for consumption purposes and are not recognized as a formal income from mortgage dedicated funds such as INFONAVIT and FOVISSSTE nor commercial banks.

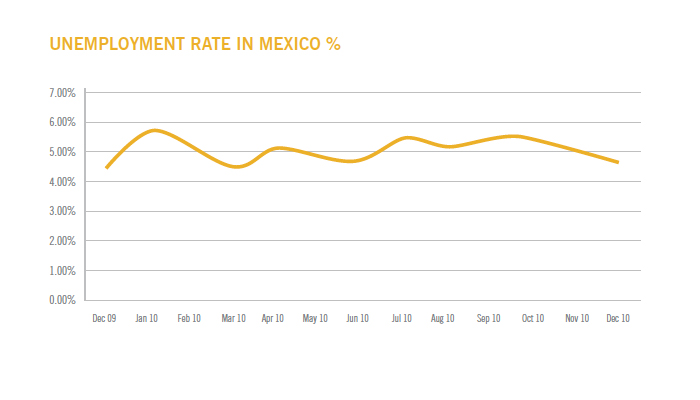

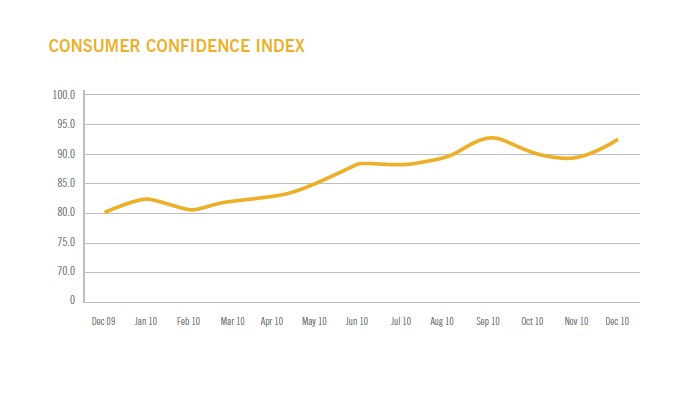

Mexico’s domestic sector showed important signs of a strong revival, supported by an improvement in the unemployment rate which decreased in December 2010 to 4.94 percent

from a yearly average of 5.41 percent, where 730,348 formal jobs (registered at Mexico’s social security institute) rebounded from 2009 levels. The overall recovery of the formal labor market led Mexico’s consumer confidence index to rise more than expected in December to its highest reading in three months, 91.2 basis points compared to 80.1 basis points as of December 2009.

Employment growth, consumer confidence and a more dynamic consumption trend translated into an increase in productivity at the end of the year and reflected in Mexico’s economic activity indicator (IGAE) which registered an improvement of 5.5 percent for the full year compared to 2009. In addition, industrial activity grew 6.0 percent as a result of the positive performance of three of its four components. The manufacturing sector led the improvement with a growth of 10.0 percent followed by an increase in electricity production, water and gas supply and the mining industry of 2.5 percent and 2.4 percent, respectively.

As important as a sustained growth and financial stability are, a stable exchange rate and inflation are important indicators in evaluating the health of a country's economy. While most emerging economies across the world are struggling to contain inflation, there are few exceptions and one of these exceptions is Mexico. The December inflation rate in Mexico was 4.4 percent, and during the fourth quarter, Mexico's inflation level increased to 4.2 percent from 3.7 percent during 3Q10, which was still below the long-term average inflation rate of 5.1 percent since 2000. On the other hand, during 2010, the peso/dollar exchange rate remained below Ps.12.50 per 1 US dollar, registering a year-end exchange rate parity of 12.38 pesos per U.S. dollar as of December 2010.

All in all, and as a reflection of the previously discussed factors, during the fourth quarter, Mexico’s GDP grew by 4.6 percent, resulting in a yearly growth rate of 5.4 percent compared to a plunge of 6.5 percent during 2009 due to the global recession.